Associated Builders and Contractors reported today that its Construction Backlog Indicator inched up to 8.5 months in November from 8.4 months in October, according to an ABC member survey conducted Nov. 20 to Dec. 4. The reading is down 0.7 months from November 2022. View ABC’s Construction Backlog Indicator and Construction Confidence Index tables for November. View the full Read more

economy

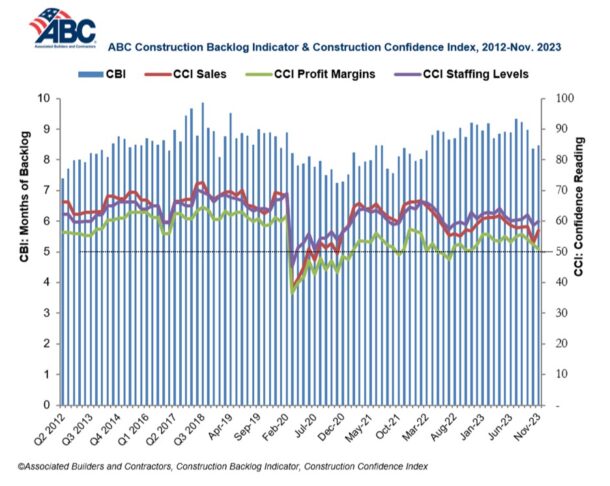

Associated Builders and Contractors reported today that its Construction Backlog Indicator inched up to 8.5 months in November from 8.4 months in October, according to an ABC member survey conducted Nov. 20 to Dec. 4. The reading is down 0.7 months from November 2022.

View ABC’s Construction Backlog Indicator and Construction Confidence Index tables for November. View the full Construction Backlog Indicator and Construction Confidence Index data series.

Despite the monthly increase, backlog is currently 0.8 months lower than at July’s cyclical peak. The sharpest declines over that span occurred among contractors with more than $100 million in annual revenues, who collectively reported fewer than 10 months of backlog in November for the first time since the second quarter of 2018.

ABC’s Construction Confidence Index readings for sales and staffing levels increased in November, while the reading for profit margins fell. All three readings remain above the threshold of 50, indicating expectations for growth over the next six months.

“A growing number of contractors are reporting declines in backlog,” said ABC Chief Economist Anirban Basu. “The interest rate hikes implemented by the Federal Reserve appear to be making more of a mark on the economy. Not only has the cost of capital risen over the past 20+ months, but credit conditions are also tightening, rendering project financing even more challenging.

“The good news is that certain interest rates have begun to fall in anticipation of Federal Reserve rate cuts next year, perhaps as early as the first quarter,” said Basu. “Still, 2024 is poised to be weaker from a construction demand perspective for many firms, especially those that depend heavily on private developers. Those operating in public construction and/or industrial segments should meet with less resistance on average.”

Note: The reference months for the Construction Backlog Indicator and Construction Confidence Index data series were revised on May 12, 2020, to better reflect the survey period. CBI quantifies the previous month’s work under contract based on the latest financials available, while CCI measures contractors’ outlook for the next six months. View the methodology for both indicators.

Growth bolstered by an increase in price points despite material shortages and higher labor costs The National Kitchen & Bath Association (NKBA) – the world’s leading non-profit trade association for the kitchen and bath industry providing tools, research, certification, and events to thousands of professionals – has released its Kitchen & Bath Market Index (KBMI) for Q1 Read more

Growth bolstered by an increase in price points despite material shortages and higher labor costs

The National Kitchen & Bath Association (NKBA) – the world’s leading non-profit trade association for the kitchen and bath industry providing tools, research, certification, and events to thousands of professionals – has released its Kitchen & Bath Market Index (KBMI) for Q1 of 2022. The quarterly report, which is aimed at measuring the health of the kitchen and bath industry, found that the industry enjoyed a successful opening quarter of the year, growing 12.6% in Q1, with industry professionals expecting further growth as the year continues.

“Despite a number of ongoing economic hardships, from material shortages to higher labor costs, we’re excited to see our industry continue to grow and be optimistic about the future,” said Bill Darcy, Chief Executive Officer, NKBA. “As the world shifts toward a new normal, we’ve seen the kitchen and bath industry continue to adapt to the times by evolving e-commerce practices, stocking up on available products, and turning toward historically underutilized brands to fulfill customer needs.”

While price points have continued to rise, demand for remodeling projects has stayed strong, enabling the industry to continue to grow in the new year. In the KBMI Q1 report, all kitchen and bath industry segments reported high single-digit sales growth year-over-year (YOY) except for manufacturers, who reported double-digit sales growth of 10.3%. Not only were sales numbers up compared to 2021, but quarter-over-quarter (QOQ) sales accelerated for all segments of the industry.

2022 full-year sales growth expectations have also increased after a successful first quarter, with professionals anticipating +15.1% growth for the year, up from the 9.4% reported just three months ago. In the latest KBMI report, the kitchen and bath industry rated future business conditions a 78.6 on a 100-point scale, displaying cautious optimism about the future of the industry. Rising interest rates and low resale inventory have been tailwinds for big remodeling projects as consumers leverage home equity and other discretionary income to ‘trade up in place.’ Despite additional inflationary pressures potentially pricing out some homeowners, the industry reported a healthy number of backlogged projects, allowing the sector to feel confident about the road ahead.

“From manufacturers and designers to contractors and retailers, the entire kitchen and bath industry has had to adjust to the ever-evolving times that we live in. Despite the ongoing headwinds and potential unknown challenges ahead, all signs currently suggest that 2022 will be another strong year for the industry,” continued Darcy.

Among the report’s key findings were:

- Material Shortages Cause Delays and Cancellations: As the ongoing worldwide material shortage continues, kitchen and bath industry professionals have reported serious delays to their projects. Forty-three percent (43%) of building and construction firms report most of their projects were behind schedule in Q1 2022. Firms have tried to get out ahead of projects by pre-ordering as often as they can, however, industry-wide backorders and shipping delays prevent them from maintaining timelines. A further consequence of these material delays has been client cancellations due to long timelines, as 46% of building and construction firms had clients cancel and/or postpone projects in Q1. While this is a slight improvement from Q4 2021’s 50% cancellation/postponement rate, the trend continues to be a concern for the industry moving forward.

- Luxury Products In Demand, Come With Longest Lead Times: The KBMI for Q1 2022 found that luxury products once again are the most popular category for consumers. However, these products also come with the longest wait times. An increasing number of industry professionals (55%) report differing lead times across luxury, mass market, and entry-level products/materials. Seventy-nine percent (79%) of those indicating a difference say lead times for luxury products/materials are the longest. Consumers choosing to move forward with big project remodels are often opting for high-end products, associating quality and durability with the higher price tag.

- Labor Remains Elusive and Expensive: Industry professionals reported labor availability as having a significant impact on their businesses and their ability to keep up with demand, rating the overall impact a 6.7 on a 10-point scale. Industry professionals continue struggling to find qualified labor, raising rates by 18% on average to retain and/or attract talent. Seventy-six percent (76%) of designers are increasing labor rates 21% on average to retain existing employees, saying competition for qualified labor is fierce.

To learn more, visit here.

Projects Shift Upward in Price Sales growth expectations rise to 13.4% The National Kitchen & Bath Association (NKBA) and John Burns Real Estate Consulting (JBREC) today reported that their Q1 2021 Kitchen & Bath Market Index (KBMI) has soared to a rating 79.8, its highest score since the inception of the index. KBMI measures the Read more

Projects Shift Upward in Price Sales growth expectations rise to 13.4%

The National Kitchen & Bath Association (NKBA) and John Burns Real Estate Consulting (JBREC) today reported that their Q1 2021 Kitchen & Bath Market Index (KBMI) has soared to a rating 79.8, its highest score since the inception of the index.

KBMI measures the current strength of the industry, expectations and challenges facing four major sectors — design, manufacturing, retail and building — with scores above 50 indicating expansion and scores below 50, contraction. The current rating marks an increase of 14.8 points from last quarter alone and a 38.8 point improvement from this time last year.

Significantly, one in three designers noted that clients are now requesting higher-priced products and finishes such as modern kitchen hoods or copper sinks. The trend is likely owing to quick-fix, pandemic-driven DIY projects running their course and being replaced by serious makeovers to accommodate new lifestyles.

“There is continued optimism in the industry with COVID-19 becoming less of an obstacle due to the rapid vaccine rollout,” said NKBA CEO Bill Darcy. “We are encouraged to see the index reach a historic high, and look forward to the continued industry growth as homeowners opt for larger, more upscale remodels.”

“As consumers experience more flexibility in their working arrangements, there’s an increased need for total reconfigurations for their spaces,” notes Todd Tomalak, Principal of JBREC. “And from an economic perspective, we’ve seen Americans utilizing their stimulus checks and savings from canceled vacations or other activations — which have been largely paused for the last year — for these home-improvement projects.”

Overall, demand is at an all-time high as vaccination rates increase and for some, permanent and hybrid work-from-home lifestyles are encouraging consumers to reconfigure their home layouts. As the pandemic’s impact on the market starts to lessen and previously postponed projects resume, backlogs for projects are reaching upwards of three to six months. Continued supply chain disruptions from COVID-fueled demand and factory shutdowns at the onset of the pandemic are further affected by the Suez Canal incident and overall port congestion, but NKBA members remain confident in the industry outlook with expected sales to be markedly higher in Q2 2021.

As members see less of a negative impact from COVID-19 on their business, they reported a near-double-digit sales growth of 9.7% on average in Q1 2021, compared to the same period in 2020.

As for future sales and overall industry health, bullish demand and consumer confidence continue to fuel a positive outlook. Design companies have the lowest rating of the overall industry, at 76.1, while Building & Construction, Retail Sales and Manufacturing segments soar at 83.8, 82.2, and 86.7, respectively.

And overall, the industry increased full-year sales growth expectations to 13.4% in 2021, up from their rating of 10.7% in Q4 2020.

The following trends are expected to impact homeowners and the industry through 2021:

- Members are seeing larger project scopes as homeowners invest in whole-home reconfigurations and luxury finishes.

- Designers also cite permanent work-from-home lifestyles as a catalyst for the consumer shift to high-end, higher-priced materials and finishes with designer firms reporting a 61% increase in the average size of projects.

- The main obstacle for members is sourcing affordable materials as delays and price hikes make it difficult to maintain profit margins. More US-based sourcing could be likely as import delays and pricing become more severe and firms are sourcing outside their approved vendor list to accommodate.

- Appliances have been the most difficult products to source, with 51% of designers reporting difficulty sourcing refrigerators, ranges/stoves and dishwashers.

- The majority of firms are increasing labor rates to maintain current staffing levels and bolster recruitment efforts, but these increased costs aren’t expected to deter demand, as consumers are eager to remodel their primary bath and kitchen spaces.

Notable challenges and opportunities for the kitchen and bath market include:

- Over half of designers (55%) report no project cancellations or postponements in Q1, but 45% note material shortage and product pricing are starting to affect project timelines.

- As vaccination rates climb, consumers are more comfortable shopping in-person for items with over 50% of retailers reporting growth in foot traffic in Q1 2021 (compared to 35% in Q4 2020).

- 45% of retailers continue to report a shift in price-point with 70% shifting to higher prices, and despite price surges for some products, consumers are still opting to pay for high-end products and finishes. Refrigerators and ranges/stoves are seeing the highest price climb at 12% and 11%, respectively.

- 60% of manufacturing firms report average lead times of 6+ weeks in Q1 2021, a drastic increase from Q4 2020 (36% reporting 6+ week lead times). 78% of manufacturers report severe capacity constraints at this time, a rise from the prior quarter (23%) due to extended lead times on raw materials and significant freight delays.

- With the surge in remodeling demand, 67% of building and construction firms report a backlog of 3+ months and of that, 21% have a backlog extending through 2021.

- With the pandemic affecting many industry professionals, the already strained labor market continued to dwindle. In response, over 60% of companies report increasing labor rates to retain current staff and of the companies reporting labor rate increases, almost half report increasing labor rates 10-19%.

Nearly Half of Industry Professionals Saying Demand Has Returned to Pre-Pandemic Levels Today, the National Kitchen & Bath Association (NKBA) and John Burns Real Estate Consulting (JBREC) released their Q4 2020 Kitchen & Bath Market Index (KBMI), which shows industry sales grew 2% from Q3 2020 and 4% year-over-year from Q4 2019. Retail sales are experiencing especially impressive Read more

Nearly Half of Industry Professionals Saying Demand Has Returned to Pre-Pandemic Levels

Today, the National Kitchen & Bath Association (NKBA) and John Burns Real Estate Consulting (JBREC) released their Q4 2020 Kitchen & Bath Market Index (KBMI), which shows industry sales grew 2% from Q3 2020 and 4% year-over-year from Q4 2019. Retail sales are experiencing especially impressive growth, with average sales up 7.9% from last year, followed by manufacturing (5.5%), building/construction (3.8%) and design (2.4%).

The KBMI reached a rating of 65, representing a third consecutive quarter-over-quarter increase. The index stood at 61.9 in Q3 2020 and was below 50 in both the first and second quarters of last year. Scores above 50 indicate expansion and scores below, contraction. All indicators of this report have improved over the last several quarters — with kitchen and bath market respondents ranking current conditions at 59.8; future conditions at 72.7; and the health of the industry (measured on a scale of one to 10) at 7.1, just below the pre-pandemic 7.2 registered in Q4 2019.

Supply-chain disruption, cost of materials, concerns around keeping COVID-19 under control and availability of skilled labor are the top concerns of industry professionals. More than half (56%) say COVID-19 has worsened the pre-existing labor shortage by fueling demand, with 58% reporting their pipelines are larger now than at the same time in 2019.

The industry expects 10.7% sales growth in 2021

The NKBA has identified the following consumer trends via the latest KBMI report:

- The shift to smaller project sizes seen earlier in the year reverses, as homeowners are undertaking larger projects, including expanding and rearranging floorplans or creating dedicated offices, to increase home functionality. This recalibration of priorities is contributing to anticipated business growth across sectors, as more complex jobs require a level of professional help not seen in 2020’s DIY boom.

- In fact, pandemic circumstances are actually driving demand to 60% of kitchen and bath companies, with members reporting that consumers are beginning the remodeling projects they planned while sheltering in place in 2020.

- Still, there remains higher demand for lower-priced products and finishes. Homeowners also seek out wellness design, perhaps unsurprisingly given the focus on physical and mental health spurred by the pandemic.

“We’re seeing an incomparable surge in homeowners looking to rearrange floor plans, tear out complete kitchens, baths and other rooms to make space for increased activity within the home, and generally create a space that better suits their evolving needs,” said NKBA CEO Bill Darcy. “Our industry’s greatest challenge will be operational, as our members aim to meet growing demand from homeowners with an unmatched appetite for remodeling.”

Each sector of the kitchen and bath market is impacted by current demand in different ways, though all report supply-chain disruptions as a significant, negative impact of COVID-19 on their business. Other key takeaways include:

- Retail sales see strong growth across all price points, though wood items like cabinets are under inflationary pressure due to the lumber market. Regardless, retailers have the most positive outlook on the industry, ranking the KBMI highest of any group at 71.7.

- Demand continues to exceed supply for manufacturers, most notably in cabinetry and appliances, but fewer than one in five (19%) say supply-chain disruptions are significantly impacting their business.

- Building and construction firms report cancellations and postponements are declining, with more than half (58%) reporting zero in Q4, compared to 49% in Q3. Builders are more likely to report supply-chain disruptions as significantly impacting their business (23%) compared to other sectors.

- Half of designers say demand for future projects is higher than it was pre-COVID, while consumers’ finances have less of a negative impact as economic confidence has continued to improve over the last several quarters.